Discover essential FX hedging strategies and currency management best practices from our foreign exchange experts.

The Power of Simulation

According to French futurologist Jacques Attali, the next big wave in business process innovation will involve simulation:

“Digital mock-ups can be made of buildings, stadiums, hospitals, neighborhoods, cities, freeway networks or roads, before they are even built. We also digitally simulate clothes, medicines, factories, airplanes and weapons.” — Jacques Attali.

But what is the value of simulation technology in Currency Management Automation? In this blog I spell out the role of simulation in terms of the steps taken by companies to assess the need for automated FX solutions:

- Real trades analysis

- Synthetic data generation

- Monte-Carlo simulation

- KPIs for different hedging programs

- Return on Investment

The power of simulation: analysing real trades

To help corporate FX risk managers assess the value of Currency Management Automation, we provide them with a numerical estimate of the benefits they obtain. To accomplish that, we need simulation technology.

For firms that do not systematically hedge the FX exposure, the results of simulation can be pretty surprising. This is because many scenarios —and not one or two lucky ones— can be tested. But it gets more interesting when companies do hedge.

As managers provide us with their real trades, FX policies can be thoroughly backtested with simulation tools. This makes it possible to show divergences between a firm’s stated policy —for example, layering— and what its managers are really doing.

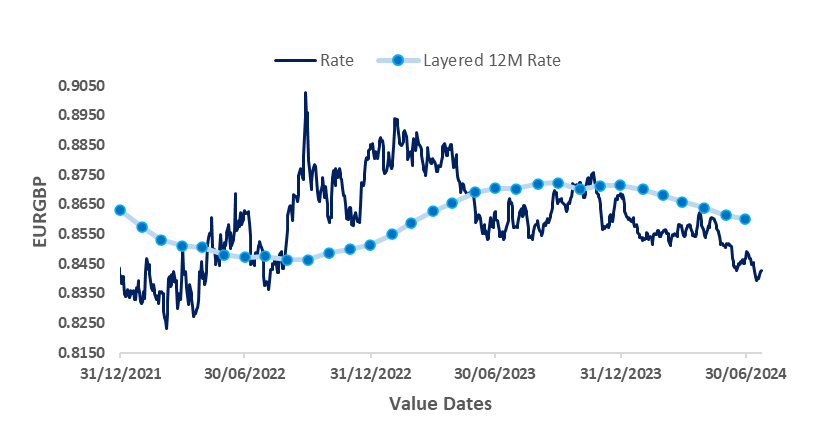

The illustration below shows several trading patterns. Program 1 and Program 2 are both structured and well-performing layered programs. But real trades display no systematic and organised trading pattern, i.e., no regular stairs in terms of time and size.

The firm in question is unlikely to reach its stated primary objective of achieving a smooth FX hedge rate over time (*). But what if the data is not even available?

In this case, simulation makes it possible —under certain circumstances— to generate, at least in part, the missing data. This synthetic data mimics different business patterns in terms of seasonality, frequency and volatility.

A four-step method to arrive at an ROI

What happens next can be summarised in the following four steps:

1. Setting the relevant parameters

To arrive at the program that best fits the firm’s FX goals, special attention is paid to:

- The company’s pricing parameters

- Managers’ tolerance for risk

- The forward premium or discount in currency pairs

This information is needed to recommend a program: micro-hedging, static hedging, layered hedging or a combination. It is also required to calibrate the program when setting markups and deciding to anticipate or delay hedge execution.

2. Back-testing

To assess the robustness of the FX program, at least five years of past market data are used. In relation to the program setup, specific parameters are fine tuned, such as the budget rate or the markups.

It’s about testing the robustness of companies’ FX hedging programs. If managers think that five years are not representative, we can proceed to stress test the FX program with Monte-Carlo simulation.

Monte-Carlo simulation tests hundreds of FX rate paths that are randomly generated through a financial stochastic process tuned according to past historical data. They provide a consistent answer about the value of a proposed FX hedging program.

3. Key Performance Indicators.

The value provided by the proposed hedging program is assessed with numerical KPIs. Quite naturally, these KPIs depend on the type of program. Simulation makes it possible to display ‘insane’ levels of KPI-related granularity, including:

- All programs. Number of entries, number of trades,FX volume traded

- Micro-hedging. P/L impact, forward points impact, average number of entries per trade

- Static hedging. Weighted Average Hedge rate, forward point impact, unwound amount

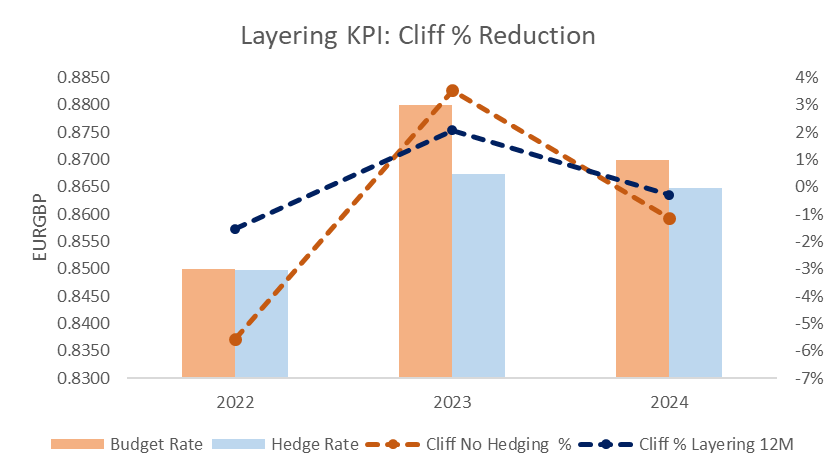

- Layered hedging. Cliff range, Weighted Average Hedge rate vs market rate

4. Return on investment

Finally, a ROI is assessed on the basis of the numerical impact of the proposed FX hedging program. This is based on the relevant KPIs, although some items like the benefits of automation may be more difficult to quantify.

Do you have a robust FX risk management solution in place? Send us a sample of your data, alongside the objective of your FX hedging program, and we’ll assess it. 👉 Send us your data and FX challenges here.

(*) Note that Program 2 includes conditional orders to delay hedge execution with unfavourable forward points. Depending on the currency pair and on the size of the exposure, delayed hedge execution translates into enormous savings.

.png)